Fertiliser prices creeping up as spring buyers return

Fertiliser prices are increasing again after the autumn lull as spring buyers become more active and supplies appear to be tightening.

A more positive outlook for grain prices, a narrowing window before the main usage date, and generally good-looking crops have all spurred buyer activity, and global fertiliser prices are firming in response.

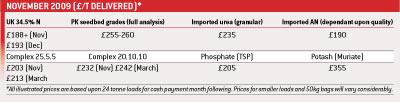

Egyptian urea, for example, has risen from $235/t f.o.b. to $285/t, meaning that replacement costs – the amount an importer has to pay to “replace” material already in stock – for urea on-farm are around £235/t.

In addition, it is estimated that this season’s nitrogen market will be 300-400,000 tonnes greater than last year, leading to a total nitrogen market over 2m tonnes. Stocks are reportedly low at GrowHow sites, with planned maintenance shutdowns in January. At the same time Polish and Lithuanian imports are declining as their AN is required in home markets. No wonder merchants are suggesting “buy now”.

NPKS compound sales are also increasingly buoyant, in part due to a forward price structure from Yara and GrowHow, listing prices through to March. The main interest is in grassland compounds where prices increase £10/t over the five months. This £2/t per month rise is well within the usual range. GrowHow once more have complex potato fertiliser (15.15.20) and oilseed grade (17.17.17) on their books, the former starting at around £277/t on farm.

The confidence to give clear compound prices stems from the stability which has emerged in phosphate and potash prices. Indecision over potash prices – the most expensive of the major four nutrients – has settled following major international dealing and muriate at £355/t on-farm, is holding firm.

Meanwhile, GrowHow’s 50% shareholder, Terra Industries of America continues to reject a proposed merger with CF Industries, one of America’s largest nitrogen producers. This is despite the fact that all three of CF’s director nominees for the Terra board were this month elected by Terra stockholders.