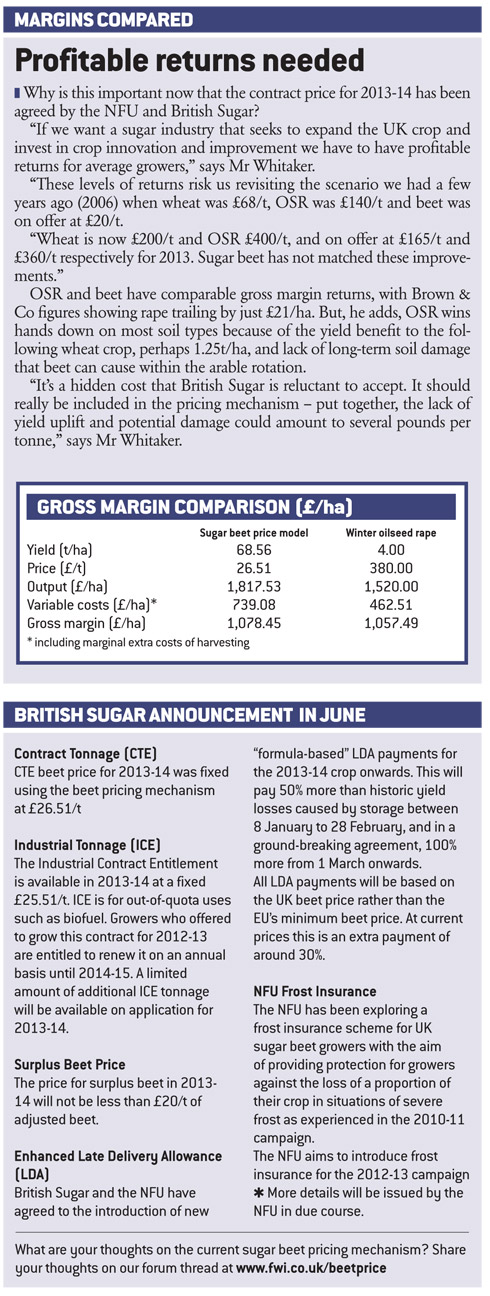

Beet margins being eroded by pricing model

Despite a recent mid-term review the sugar beet pricing mechanism is not delivering a fair return for growers, says Charles Whitaker, a partner at Norwich firm Brown & Co.

Sugar beet direct costs have risen by almost 70p/t over the year according to the British Sugar/NFU pricing model used to calculate the 2013-14 ex-farm price. Yet growers will receive £1/t less for their crop.

The key factor contributing to the fall is a £1.71/t reduction in the currency-linked variable margin element of the pricing model, says Mr Whitaker.

It offers growers 25p/t for every 1p that, during the early June reference period, sterling exceeds the 70p/€ baseline exchange rate agreed when the pricing model was established.

In the first year this margin equated to £3.33/t and rose to £4.50/t last year, but only amounts to £2.79/t for the 2013-14 season. This is eroding the grower margin at a time when costs of production are rising, says Mr Whitaker.

“Farmers are not paid in euros, nor are their competing crops/land uses paid in euros, and this is essentially a “cost” model”, with the grower’s margin only being generated by this variable margin and the wheat price (see below). It is unreasonable that such a margin is dependent on the euro; a variable that impacts British Sugar, but has no relevance to the grower at all.”

The wheat price bonus element is also failing to deliver, he believes. This raises the beet price by 5p for every £1 that the November futures wheat price exceeds £110/t during the early June reference period, but is capped at £150/t. As a result, the uplift from rising commodity prices has been limited to £2/t.

“Growers can link in to these higher commodity prices before, when and after they they sign the beet contracts. The pricing model’s upper limit does not reflect returns which are reasonable given the commodity markets and competing land use returns.”

In addition, Mr Whitaker believes the so-called “fixed uplift” used to calculate the contribution to fixed and overhead costs no longer reflects real farm business overhead costs. Its value remains the same as 2012-13.

“It cannot be right that overheads have not gone up, in agriculture of all industries,” he says. “We all know FBT rents have increased massively in the past three years. I can only assume the pricing model figures use average rent costs across the board agreed at the outset of the current Inter-Professional Agreement in 2010.

“If we are seeking a fair and full calculation of the beet price then we have to reflect current rental costs of land.

“Why should we still be using the historic cost of land, or rental values? Rental equivalent is too often understated – it should reflect a current and realistic annual rental value for land, the baseline of which is being impacted by readily available bids to grow other crops with less risk such as maize for anaerobic digestion plants, which can provide £150-200 an acre to the land provider – more than the total overhead contribution used in this model.”

He describes the mid-term review of the IPA as a missed opportunity. “There can be no justification for a cost of production-based pricing model actually resulting in a falling beet price when costs have risen,” says Mr Whitaker.

“It is time for a rethink about the share of the cake if we are to “work together” to grow the beet industry as its clear that the 2013 contract on offer is somewhat less than it could be.