Can Group 1 milling wheat still bring in the bread?

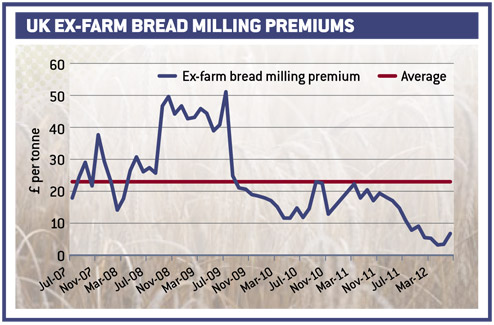

Milling wheat premiums plunged to their lowest level for five years this spring, leaving many growers questioning the viability of the crop.

During April and May, Group 1 varieties were typically worth just £5/t more on the open market than out-and-out feed varieties. That wiped more than £140/ha off the typical gross margin than anyone budgeting on the past five-year average of £23/t (see graph) would have predicted, leaving these breadmaking wheats trailing feed varieties grown on similar soils.

Quality was good and yields held up better for many than had been predicted. As the season unfolded it became clear that millers were spoilt for choice.

However, rising concerns over the effects of the recent dull and damp weather on the current crop’s health, grain fill and subsequent quality have sent milling wheat premiums soaring. At the time of writing (mid-July) up to £40/t was reportedly available in the North West for November 2012 delivery, though trade was at low levels.

Contracts offering a minimum premium of £25/t over feed for new crop have been readily available. If those premiums persist further out, then milling wheat looks a good bet if recently released HGCA gross margin estimates for crops due to be sown this coming autumn are anything to go by.

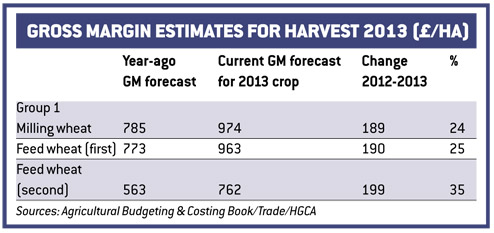

These estimates assume a breadmaking premium of £20/t, in line with the previous five-year average, and a feed wheat price of £158/t, using the November 2013 delivered value available during the week ending 6 July, says AHDB Market Intelligence senior analyst Charlotte Garbutt.

The calculations also assume a yield of 8.3t/ha for milling wheat and 8.9t/ha for feed wheat.

The gross margin for Group 1 milling wheat rose by about a quarter on the year to £974/ha, giving it a slight lead over feed wheat, which produced a gross margin of £963/ha, also a quarter more than the previous year. As well as higher market prices, lower fuel and particularly fertiliser prices helped lift the budget, with ammonium nitrate, triple superphosphate and muriate of potash forecast to fall, compared with year-ago levels, by £42/t, £65 and £175/t, respectively.

Actual premiums will depend upon quality and availability. “At the yield level we have assumed a downward move to a premium of £18.63/t would mean that milling and feed both offer the same gross margin,” says Ms Garbutt.

For their own forecasting purposes growers should use a five-year rolling average for the Group 1 premium when assessing the crop’s viability rather than judging it on the previous season’s performance alone, she adds.

“Looking back to 2007-08 the breadmaking premium has averaged £23/t, but has ranged from £50 to £5/t.”

Individual businesses should also identify the yield differential between the two types on their own farms. “This is key to determining relative economic performance.”

Variety choice is important, and growers have got better at it, says Ms Garbutt. “They are talking much more to merchants and millers to find out what they want. This goes for all wheats with milling potential. The market has become much more specific, with individual mills having particular preferences.”

A good marketing strategy is a must to realise gross margin forecasts, she adds. “It is very likely that markets will remain volatile during 2012 and 2013. There are a variety of contracts available depending on growers’ attitude to risk and how far ahead they want to sell, and there is the open market as well. If there is a shortage then millers might look to secure more supplies ahead of next harvest, so we might see some good opportunities for the 2013 crop.”

On paper at least, there seems little reason for the area of Group 1 wheats this autumn to fall below year-ago levels, when they accounted for 17% of Great Britain’s wheat area, according to the recently completed AHDB HGCA 2012 planting survey.

But, if the wet weather continues, many growers will struggle to meet full milling wheat specification and to get a decent premium from this harvest’s crop. That could yet affect growers’ decisions this autumn, says Andrew Wraith, head of agribusiness at Savills.

“Big premiums are great if growers can deliver. For the dedicated milling wheat grower who grows the crop because it suits his land, which is unlikely to be capable of delivering very high yields of feed wheat, and who is geared up to handling it to maximise quality, it will be a welcome bonus. But for anyone in the middle ground who dips in and out of Group 1 wheat, will it be enough to persuade them to grow it again if they run into serious quality problems this year?”

Higher feed wheat prices could also work against breadmaking varieties, says Mr Wraith. “The higher the price, the higher the premium needs to be to maintain the same proportional advantage. A £15/t premium when feed wheat was worth £80/t looked good. At £160/t a £20-25/t premium is not as attractive – you need £30/t.”

He believes some growers will look to reduce their risk next season. Indeed some clients have already taken the decision to cut back. “Those that jump in and out may think what’s the point, especially if quality suffers this harvest. Bushel weights won’t have been helped by the dull wet period during grain filling, and if things stay wet we could have problems with Hagbergs.”

The decision to grow breadmakers depends on what yield advantage feed wheats can deliver, which comes down to land type. Lighter soils may not be able to deliver the difference in yield needed, he says. “But better-bodied soils may well be growing more feed wheat this autumn.”

On the other hand, newcomer Crusoe, which has much better disease-resistance scores than either Gallant or Solstice, could tempt some middle-ground growers, he adds. “The arrival of a new variety often stirs interest in milling wheat, and Crusoe ticks a lot of boxes. The yield statistics look good too, so if you don’t make the full premium you won’t be so badly off.”

There is also a chance that premiums will strengthen further over the next few weeks, which could persuade growers to put more milling wheat into drills this autumn. “Growers should examine the premium they need in their own land. They should then look at their strike rate. If they only manage to get 75% in at full spec, then they will need a correspondingly larger premium.”

In 2011/12, growers with contracts would have had the best chances of securing a decent premium, he adds. “They will have been relieved they took that decision, and the result will probably keep them in the game. Those who sold on the open market later might be thinking rather differently.”

However, 2012/13 could turn out to be a complete reversal – the open market could offer the best premiums if the shortfall is realised, he notes. “It could pay to rethink the marketing strategy.

“Nevertheless, if a miller is offering a minimum non-defaultable £25/t premium over feed contract, I’d suggest growers ought to lock in at least some of their tonnage as that should more than cover the additional growing costs.”