Farm Finance: Manage cash flows to cope with the crunch

A combination of factors over the past six months has put some farming businesses under extreme pressure, with the levels of working capital required higher than the late 1990s and early 2000s, when farm profitability was at a low point. But now this pressure comes in the context of a downturn in the wider economy, which has direct implications for the farming industry.

World economic factors, financial instability in the UK and world banking sector and the weather have all had an impact on both output and farm costs, and, therefore, on cash flow.

Improved cereal prices of harvest 2007, due to the world supply and demand imbalance in grains, were a saviour for some, but a burden for others. At some point most arable farmers benefited from higher prices, which more than compensated for a below-average yield. For the livestock sector, however, this was a burden, with costs increasing for any feedstuffs based on cereals, maize or soya. This created a difficult period for some livestock producers, most notably those in the pig and poultry sectors.

The sea-change in world supply and demand dynamics of bumper yields, increasing stocks and reduced market speculation as a direct result of the financial crisis all led to prices falling dramatically. Overnight all optimism in the UK arable sector disappeared and many farmers exacerbated their cash-flow problems by refusing to sell at today’s prices.

The wet and late harvest led to later-than-usual grain sales and a lack of cash to cover fuel, fertiliser, chemical and contracting bills. For some the wet harvest led to serious crop write-offs, which will be disastrous for cash flows.

Although the oil price has now fallen back from its peak, that spike came as most farmers were buying for the season ahead. The cost burden is now being carried in many trading accounts. Many farmers also found themselves forced to make their fertiliser purchases after prices had leapt dramatically some businesses could be looking at a 150% hike in fertiliser bills.

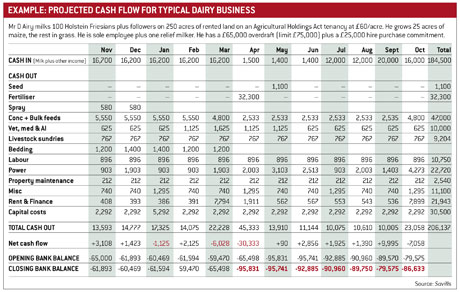

Farmers must now have more working capital tied up in growing crops or producing livestock than ever before, and to survive, careful management is required. History suggests that farming has performed well during previous recessions. But the credit crisis is a new one and the cause of this economic downturn has hit farmers as hard as everyone else. This includes those who invested heavily to generate diversified income – for example, from farm shops – as consumers rein in spending on luxuries and leisure activities.

Farm borrowings generally stand at an all-time high. Latest Bank of England figures show agriculture and fishing debt standing at historic highs and 9% higher than it was in the last quarter of 2007. Although the industry as a whole does not have a gearing problem, the availability of further borrowing at realistic rates may prove difficult for some farming businesses. It remains to be seen whether the Bank of England’s recent interest rate cut is passed on in full to the consumer. If not, we may well be moving into a period where, unless credit is already secured or cash is available, the ability to make decisions within a farming business will be limited.

Single payments

The payment window opens from 1 December. If you have been notified by the Rural Payments Agency of any queries on your claim, reply promptly and chase the issue up to conclusion. Outstanding issues on a claim could and probably will delay the payment. Being paid in December or June will have a significant difference on cash flow.

Bad debts

The risk of bad debts through payment defaults is as high as it has ever been. So include credit checking, bad debt insurance, advanced payments and tight debtor control in your strategy.

Avoid surprises

Beware of unexpected payments. It is easy to forget those that are unrelated to the day-to-day business, like Hire Purchase repayments. Have you bought anything on credit which had a payments holiday, and for which repayments will soon begin? Also beware – companies and individuals may look to take advantage of financial difficulty. Any deal that seems too good to be true probably is. Always read the small print and seek advice.

Tax bills

Many farming businesses will have an income tax liability in January 2009, following some reasonable profits in the last financial year. It is essential to make a provision to pay this and to plan for future tax liabilities.

Offset risks

Poor financial planning has led to some farmers becoming victims of their own making. In June 2008 for example, nitrogen fertiliser prices were rising rapidly and there were questions over availability. While many ordered fertiliser, few reduced the risk by selling grain hoping prices would return to their earlier peak.

Cash flow protection tips

Budget, plan and benchmark

Have a strategy for buying inupts and selling grain or stock

Review cropping area Ð strip out marginal acres

Are livestock manures taken fully into account when assessing fertiliser need? I

Target fert and agrochemicals more accuratley with higher efficiencies of application?

Care for kit: Are tractor tyre pressures set right? Do implements match tractors? Cut out unnecessary ÒrecreationalÓ cultivation

Has the higher cost of borrowing been factored into crop marketing Ð e.g. An early grain sale with a later call option allow you scope to catch a market rally but bring some income certainty

Explore alternative animal feeds and bedding materials