Global drivers for high agri-commodity prices

Higher food and agri-commodity prices are here to stay for the next three to five years, Thos Gieskes, chief executive officer of Rabobank Australia and New Zealand, told the International Farm Management Association Congress in Methven, New Zealand. “But so is volatility.”

But what are the key drivers? Mr Gieskes outlined the six most significant drivers of supply and demand in the global market, and how they fed into higher pricing and increased volatility.

1. Intense battle for area in US

• Major competition between four main crops – maize, soya beans, wheat and cotton – for area

• Low world feed stocks – can production increase to rebuild stock levels?

• Rabobank estimates the US needs to add 7 million acres of land to increase stock levels to put supply in control

• Over past 15 years, fluctuation in area is usually 1-2%; need 3% increase to reach target

• Bioethanol demand for maize puts further pressure on feed stock rebuilding, resulting in higher prices

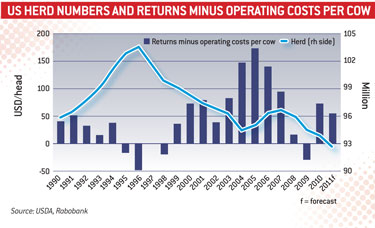

2. Beef production in US

• Cattle herd size has been declining for 15 years

• Only increases when price is above $100/head

• Higher maize prices increase beef production costs; takes returns below $100/head and no incentive to build herd numbers

• US will not increase global meat production

3. Beef being displaced in Brazil

• Prolonged growth means cost of production rising fast

• Demand for growth is putting more land into production

• Pressure on environment and high land prices

• Second largest producer of beef in world/largest exporter

• Cattle finishing less lucrative than cropping

• Same amount of cattle in traditional south concentrated into smaller area at higher cost/technological demand, and creates upward pressure on prices

• Growth areas in north/north-west Brazil

• Lower-cost production, but greater logistical challenges to transport also adds to picture of higher prices

4. China demand for feed grains

• Population and income growth is increasing demand for protein

• Animal production moving to industrial scale means more feed required through supply chain

• Unlikely China can internally satisfy feed grain demand, so will import

• Soya imports growing exponentially, corn could follow suit

• Another pull on reducing stocks, and likely to increase prices

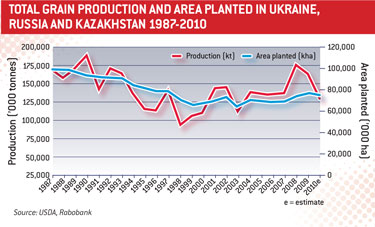

5. Unrealised potential in Black Sea countries

• Russia, Ukraine and Kazakhstan have large land availability for grain production

• But, from 1987 to today, area planted has fallen

• Volatility in climate makes production outcome unpredictable

• Technology can overcome, but needs investment and political stability

• Higher prices make investment more rewarding

• Export ban makes production environment less appealing

• Adds to complexity and volatility in world markets

6. Indian demand for dairy

• Increasing demand for dairy products

• Indian dairy plan targeting domestic production of 180 million tonnes by 2020

• Ambitious and will need investment to reach target

• Prices in India will have to increase to trigger investment

• Likely to be in global market to buy on and off to stay in line with demand in interim

The result?

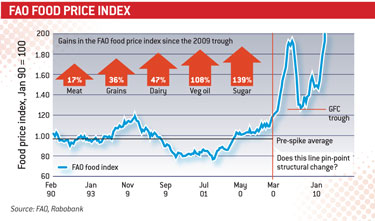

High global food prices

• Food prices relatively stable until 2000

• Increased demand from Asia saw gradual increase

• Spike in 2008 followed by global financial crisis crash

• Recent price increase from weather-related supply issues

• But is a permanent change for next few years

• Four key drivers: supply, demand, speculators and trade protectionism, and uncertainties such as climate change, currency

Volatility

• Dramatic variability in pricing disrupts margins

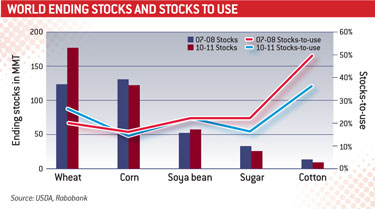

• World stocks, except wheat, significantly lower than three years ago

• Low stocks means little chance to absorb weather-related production issues or big changes in world markets

• Lack of free trade increases volatility

• Government intervention adds to complexity. For example, different import tariffs on bilateral trade agreements

• Speculators enter markets when they see potential

• Able to ride with market

• Add liquidity to market

• But exit when other markets offer greater returns

Conclusions

Agricultural commodity markets becoming more complex due to:

• Links between grain and protein production

• Weather and climate risks

• Biofuel demand linking to oil markets

• Role of governments (eg, export bans)

• Prices will be strong for three to five years

• Driven by tight supply

Increasing volatility from:

• Tight supply

• Dependence on supply from regions with variable climate

• Speculator actions

• Government intervention

Farmers Weekly wishes to thank Agrovista and John Deere for their support in attending the IFMA Congress