Tax rates on car benefits rise in 2012

The rules governing cars used within a business have changed radically in recent years – and are set for another overhaul in 2012. Catherine Vickery, tax planning manager at accountant Old Mill, explains.

Company and business cars have always been a focal point for HM Revenue & Customs, and have now taken on an important political aspect. Green issues are driving tax changes, in an attempt to change drivers’ behaviour and reduce pollution.

However, companies, sole traders and partnerships are treated very differently, with the provision of company cars becoming increasingly expensive. As a partner or sole trader, a proportion of all vehicle expenses (fuel, insurance etc) are put through the business, according to how much business usage there is. Capital allowances can be claimed for the purchase of a car, again, apportioned to the business element.

The problems start to arise where cars are held within a company or provided to an employee, as the recipient is taxed as a benefit in kind if they incur any private usage at all. This includes commuting to work, unless the vehicle is a van, when commuting is classed as a business expense.

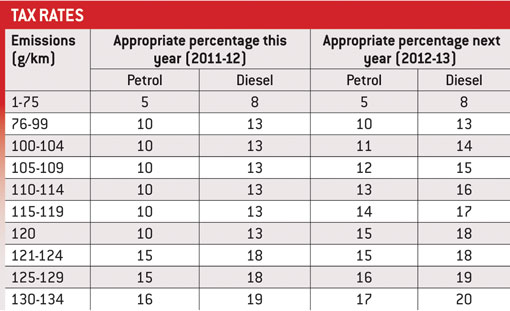

The tax rate is determined by the vehicle’s carbon dioxide (CO2) emissions and list price, with all diesel cars suffering a 3% weighting, as they emit more pollutants. The charges are changing from April 2012, making the tax rates even more onerous (see table, below). Cars with no CO2 emissions – usually electric cars – will incur no tax until April 2015.

The biggest tax hike affects vehicles with emissions of 120g/km, which will jump from a 10% tax rate to 15% next year. Take, for example, an employee driving a petrol car which is only worth £5,000 but has a list price of £10,000, with emissions of 120g/km: not unrealistic for a small company car. The tax charge will rise from £1,000 (10% of £10,000) this year to £1,500 (15% of £10,000) next year – a huge leap in percentage terms.

In addition to this levy on the car user, employers must stump up Class 1A national insurance at 13.8% of the taxable rate. And where the employer also pays the cost of fuel for private journeys, the tax rates have really rocketed, potentially adding £3,760 of taxable benefit each year. It is therefore far more cost effective for most employees and company directors to pay for their own private fuel.

Drivers who use their own cars for work purposes may now be reimbursed at 45p/mile up to 10,000 business miles a year. This is usually the most tax efficient way to use a car in the business – evident in the slump in company car offerings.

Businesses must also consider the impact on capital allowances when choosing which car to buy. Cars with emissions lower than 160g/km attract standard annual allowances of 20% (reducing to 18% from April 2012); above that threshold they receive just 10% (8% in 2012). New cars with emissions lower than 110g/km, and fully electric cars, qualify for 100% first-year allowances until April 2013.

From a tax perspective there are clearly very good reasons to opt for greener business vehicles, and given the current costs of fuel, it makes good sense all round.

• For more information, contact Catherine Vickery at Old Mill on 01935 709 381.