US poultry sector needs to reform

US chicken production is in dire need of reform if it is to compete with foreign and domestic competition, as Andrew Watts reports

The US chicken meat sector is encountering a wave of permanent, rather than cyclical, challenges that are set to drive processing into the hands of fewer, larger players.

The challenges are complex and multi-faceted, ranging from the rise of South American competitors to a maturing of domestic demand at a time when important export markets, such as Russia, are reaching self-sufficiency, says a recent report from Dutch bank Rabobank.

Increasing levels of regulation and several recent court rulings that make it difficult to reduce production, even at this time of oversupply, have also contributed to the problems.

The rise of ethanol production, which has tripled corn (maize) prices in recent years, is also cited as a threat to margins.

According to Rabobank, the world’s largest lender to agriculture, the US chicken industry is currently enduring its second major downturn in just three years. “The industry cannot continue to weather such periods of significant loss every two to three years. There is simply not enough time to rebuild balance sheets,” warns the bank, highlighting that three household names in the US chicken meat industry – Sanderson Farms, Pilgrim’s Pride and Tyson – have cumulatively lost $482m in operating profits since April 2011

Changing demand

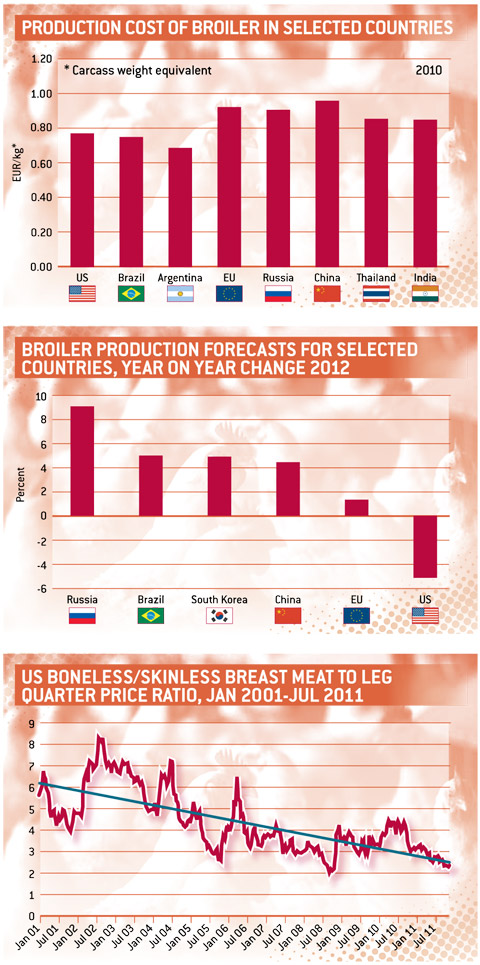

It sees the dawn of a new era, where the US model of producing boneless/skinless breast meat as the primary output is less viable. The focus on larger birds, which offer lower-cost breast meat destined for the domestic market, is ill-suited to what Rabobank sees as future demand.

Since 2001, and again with the economic decline post-2008, growth in the food service industry has waned and white meat consumption has levelled off. As US population demographics have shifted towards Hispanic and Asian consumers, and shoppers have looked for better value, so domestic demand for dark meat has increased.

The larger bird favoured for breast meat production is also poorly suited to developing export markets to the Middle East that prefer smaller whole birds, more value-added products and leg quarters. Rabobank likens the situation facing the US poultry sector to that facing car manufacturers, with large plants designed for producing gas-guzzling SUVs at a time of high oil prices. “Our challenge is to understand what domestic and foreign consumers desire and will pay for in terms of product preference and form, and then develop and market products that fit these specifications.”

Noting that four processors have either declared bankruptcy or filed for Chapter 11 protection in the six months to December 2011, it sees little room for small processors in this brutal new world, which will eventuality consolidate into the hands of fewer, stronger players. It suggests that those smaller businesses devise an exit strategy now, rather than wait until their capital has been exhausted.

“Larger publicly owned companies will have to demonstrate more discipline than is currently the case among many smaller privately owned companies. This can occur as the market drives out players, as is happening today, or if companies take action on their own, through mergers and acquisitions. Rabobank is of the opinion that it is better to choose your own fate early than wait until all grandfather’s equity has gone.”

Poor vision

The bank is particularly scathing about the management of industry players, which it considers to have been been poor. It also feels the national regulator has done little to promote confidence by failing to make decisions that would set the industry up for the next generation with any certainty or clarity.

“Until now, US chicken company executives have either been unable to see or participate in the globalisation of the chicken industry. They now face a serious risk that, instead of being the hunter, they will become the hunted in the global drive to consolidate chicken production, processing and trade,” says the report.

“In contrast to the US, where regulatory burdens are rising, governments in Brazil, Russia and China are subsidising and protecting their industries. On a relative basis, this hurts US competitiveness.”

But the threats are not all external and Rabobank is clear that if the 650,000 jobs that the chicken industry supports are to be protected, then the government’s policy of subsidising ethanol production needs a re-think, as this puts an artificial floor in the market for US corn prices.

Outlook

Rabobank believes that, despite the short-term challenges, the US chicken industry is well-positioned to exploit the growing world demand for chicken meat.

The challenge for the industry is to position itself, both structurally, through integrated supply chains that produce a desirable end product, and economically, in a cost-competitive and financially sustainable manner, to participate in this growth.

Turning the corner will also require a co-ordinated and well-supported marketing campaign, something Rabobank notes has not been a priority in the past.

“The biggest market in the world is the Middle East, in which US chicken has at best a nominal position. Leg quarters are driving profitability now more than breast meat. Export markets are no longer a destination for excess dark meat; they represent the best opportunity the industry has for growth.”

Industry contraction is accelerating as declining egg sets and chick placements translate into fewer broilers being slaughtered. For the week ending 3 December the number of broilers slaughtered was down 10%, with egg sets down an average of 10% over the 10 weeks to 7 December.

While prices are forecast to rise slightly in 2012, Rabobank believes that the cutbacks seen so far will be insufficient to restore industry profitability due to the volatility of feed and the struggling economy. A simple analysis performed by the bank suggests prices may recover to $1.50 (96p) per pound in 2012, “but that would be far below long-term averages and the level necessary for an acceptable industry return on capital given the current feed cost environment”.

Consequently, Rabobank forecasts that an industry contraction of 6-7%, rather than the 5% expected, will be required to restore profitability to a sustainable level.

The Rabobank analysis for the US poultry sector could easily be applied to other sectors of the agricultural economy. The bank notes that both the US pork and beef sectors face similar challenges, with pork production on a plateau and the beef industry “undergoing herd liquidation”.

Part of the short-term challenge is to find a sustainable pricing model. Currently retailers are absorbing higher costs on beef and pork by expanding margins on chicken. Restoring margins to previous levels could help the chicken industry, but with both food service and retail customers struggling, the industry needs to take a more disciplined approach to production costs while also being prepared to hold out on pricing for its product. “This is easier said than done, but there is no alternative. The current situation is unsustainable.”

* “This is not your grandfather’s chicken industry” is published by Rabobank’s Food and Agribusiness Research and Advisory department.