Poultry profits checked by rising production costs

Although prices paid to producers for both broilers and eggs have risen over the past 18 months, the continuing high level of feed costs has kept improvements in profitability subdued.

For free-range egg producers, the better returns have reversed a three-year decline in margins over feed, but only partially. But for broiler growers, a rise in producer prices has not been sufficient to prevent margins from declining for a fourth successive year.

Over the following pages, the fortunes and prospects for all the key sectors are examined in our annual Facts and Forecasts feature. The tables and charts highlight the trends over the past 10 years, with the latest results used as a pointer for how things may unfold in the year ahead.

EGG SECTOR

During 2013 the egg industry has continued to battle with the issues that rolled over from 2012.

Feed costs have been high in historical terms, even though gently declining since the spring. The market has been out of balance – especially in colony eggs – and margins over feed are still poor.

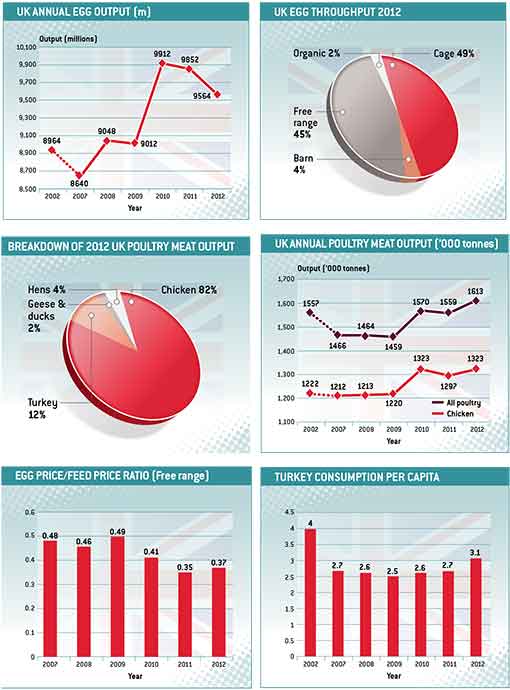

As the industry moves into 2014, the most pressing issue is still the size of the laying flock. Wholesale prices have not been strong all year and have been running below the levels of both 2011 and 2012.

Projections of chick placings indicate that the laying flock is now trending downwards, but has only just passed the point where it has cancelled the rise in bird numbers in the first half of 2012. As recently as July, the market was overloaded with eggs, and has only lately been more finely balanced.

But if the cutbacks continue at a significant rate into 2014, then the market has a better chance of strengthening during the year.

Things might have been easier if the egg sector had not expanded so rapidly during the first half of 2013. The year before, the sector had undergone a second year of falling output, and total production of eating eggs from all systems in 2012 itself fell by 3% or around 300m eggs. This was a direct result of the upheaval in the industry caused by the introduction of the cage ban at the start of the year, with too few colony units ready in time.

Yet, although the market had been very short in the early months of 2012, by the start of 2013 the market was oversupplied, and the laying flock was set to rise further, thanks to an increasing pattern of chick placing.

This guaranteed that the UK laying flock would continue growing until May 2013, preventing prices from making a stronger recovery.

In 2012 overall, day-old pullet placings had risen by 2.5 million, and the reasons for this apparently unjustified overall growth lay in the chaos in the early months of the year.

During that first quarter, total egg output in the UK was down by around 126m on the same period of 2011, a fall of 5%, and fell by a similar amount in the second quarter to reach a low point of 2,275m.

It was always going to take time to straighten out this muddle. Wholesale egg prices naturally reacted to this market and began to improve, though producer price rises were held back by retailers.

A complicating factor was the serious imbalance in the market. With free-range eggs being diverted into cage sales at a discounted price – so-called “cascading”. This further limited the extent of the price improvements that could be paid to free-range producers. Over the year as a whole, the average free-range producer price came to 97.7 p/doz, up 14p/doz.

Not surprisingly, with colony eggs in short supply, the gain in producer prices was greater, totalling 18p/doz year-on-year to average 72.2 p/doz.

In the second half of 2012, output expanded sharply as new colony units came on stream, and total production in the final quarter was up by nearly 100m eggs compared with the second. And this trend has continued throughout 2013, dominated by the colony sector.In the first nine months of this year, egg output has been up by another 5%, with the greatest increase in the second quarter. Free range also grew by 2% in the first nine months of 2013.

The improvements in producer prices have also carried forward into 2013, with the average free-range producer price in the first nine months up at 105p/doz, a gain of more than 7p/doz on the 2012 average. In the colony sector, prices have similarly risen, with the January-September average at 75.3p/doz, up 3.1p/doz.

Despite this, there has only been a small rise in profitability for the free-range sector as the cost of feed moved up in tandem. And, even though feed costs have declined substantially in the third quarter of this year, producer prices have also been trimmed on both colony and free range.

The result is that, even now, profitability is only back to the level of 2010, and well below the margins in 2009.

Examining this in more detail, feed costs had risen in 2012 for the fourth successive year and offset a big slice of the better returns. The average Poultry World layer ration price was up by another £26/t during the year as a whole, averaging £264/t, and peaking in December at just under £300/t.

The impact of this on margins over feed can be seen in the diagram above of the simple egg:feed price ratio.

Although the ratio was slightly better in 2012 than 2011 at 0.37, this was still the second lowest figure during the last six years.

This year, the layer ration price has averaged £270/t over the first nine months, which is £6/t higher than in 2012, but has still allowed an additional small improvement in profitability after factoring in the better returns. Hence the average ratio during Jan-Sept was 0.39, compared with 0.37 in 2012.

By the third quarter of this year, taken on its own, the average feed cost had dropped to £252/t, while free-range producer prices have dipped slightly to 104p/doz.

This has raised the profitability ratio once again, to 0.41, which has led to threats from the retail trade of producer price cuts as feed costs fall.

POULTRYMEAT

Poultry production in the UK has been setting new records, passing the 1.6m tonnes mark in 2012 for the first time, and expanding again throughout 2013.

In 2012, the final total of 1.61m tonnes (carcass weight), marked a 3.5% increase on the year before, and was contributed to equally by expansion in both broiler and turkey output.

This year the trend has been maintained at an identical rate, with poultry output totalling 1.23m tonnes in the first nine months of the year, a gain of 3.5%, but turkey production has slowed down.

Overall in 2012, the UK had produced another 54,000t of poultrymeat of all kinds, of which an extra 26,000t was chicken and 26,000t was turkey. Old hen meat was also up, by 3,000t, but ducks and geese were down, by 1,000t.

Over the past year the pattern has been different, with indications that the turkey sector has been taking a breather. Total output from January to September came to 126,300t, a drop of 6% year-on-year. Poult placings have been heading the same way, falling by 420,000 day-olds on the same period of last year, a drop of 3%.

Looking back over the two years, from 2010 to 2012, it is the turkey sector that has been the driving force in the market. Broiler production had remained level from 2010 to 2012 at 1,323t, whereas turkey output increased from 162,000t to 197,000t. This was the highest level of turkey production in the UK since 2004, when output stood at 207,000t.

The trend is also seen in the pattern of per capita turkey consumption over the last six years, illustrated in the chart, which shows a final bottoming at 2.5kg per capita in 2009 before rising to 3.1kg per capita in 2012. This rise has also been achieved against a background of a UK population that is rising at a rate of about 400,000 to 500,000 a year, according to World Bank data.

This year, by contrast, expansion has focused on the broiler industry where output over nine months has increased by 54,000t to 1.04m tonnes. Placings of day-old commercials have risen by 21 million in the first nine months, an increase of 3%. This expansion of the UK broiler sector appears to be set to continue for the time being.

The poultry sector has been achieving this growth despite falling margins. Although broiler contracts are meant to provide growers with stability of income, producer price rises have not been enough to cover the overall rise in feed costs over the past four years.

Average producer prices rose from 101p/kg to 117p/kg from 2009 to 2012, but the margin over feed ratio fell by 20% over that time. Growers have had to face even higher feed costs during most of 2013, so margins are unlikely to have improved.

An encouraging trend for the UK poultry sector has been the decline in imports since the start of 2012 which, combined with the extra output that year, saw the industry claw back 2.5% of market share in the UK. For 2012 as a whole, imports took 26.4% of UK domestic consumption, the lowest for three years.

This year imports fell another 10,000t during the first six months, and their market share is now down to a quarter.