Diversity could reduce your farming risk

Greater diversity of enterprises offers a way for some businesses to deal with high volatility which is now a fact of farming life.

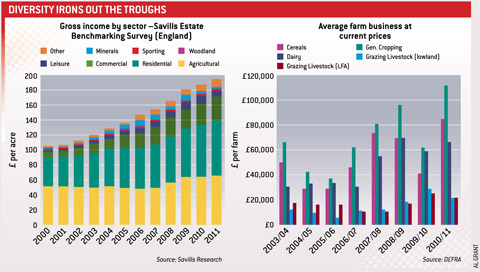

This may not mean a wholesale return to mixed farming, nor does it necessarily mean farm diversification in the traditional sense. The results of Savills’ estate benchmarking survey illustrate the steady income growth on estates with a spread of income sources (see chart below).

The survey covers about 200 estates across more than 1m acres of land in Great Britain. While gross income is growing, the shares are changing so that agriculture from let and in-hand farming now accounts for about 36% compared with 50% in 2000. Residential property income on the other hand has risen to 36% .

This contrasts with the ups and downs of individual farming enterprises shown in the DEFRA farm income data graph.

The withdrawal of price support means that volatility is here to stay, says Ian Bailey, head of rural research at Savills. Every farm business now needs to do much more than set a budget for the year – at the minimum a five to 10-year strategy is needed, he says.

“Communication between family members is key and is even more important now because the risks are greater and the change comes more quickly.”

While specialising may have been the right thing for most farms in recent decades, all businesses now need to carefully assess capital assets, resources and enterprise mix, says Savills’ Ashley Lilley.

“Is there cash potential which is not being tapped, are there assets whose value could be enhanced, is there anything you can do to spread risk?”

Business pointers:

• Scrutinise assets – some may have capacity to generate more income, others may be surplus

• Low interest rates offer an opportunity to diversify – but not necessarily “farm diversification”

• Think broadly about opportunities to collaborate – other businesses such as contract livestock rearing need land, buildings or partner farms

• Are the right resources there for non-farming income – especially skills and aptitude of people?

• Residential property is a potential investment area – buying to let, improving current housing to increase asset value/rental potential – property type and location are key

• Projects like barn conversions need careful research – market much trickier than five years ago

• Opportunities include letting buildings for storage, letting land for specialist cropping, supplying timber from woodland for fuel

• Consider investments maximise income and cut costs, eg renewable energy for heating or hot water in houses and commercial lettings, may also make use of farm timber or other raw materials/by products

• Don’t forget grants – new schemes have recently been announced, more to come

• Link succession and retirement planning to tax planning – the earlier all start, the better the chance of enhancing and preserving capital values

• Reduce or spread risk by hedging crop income and other risk management

• Livestock – sell to more than one end user, eg live and deadweight, consider fixed price contracts eg Blade Farming

• Tenants need to balance working capital requirement with capital taken out of business for pension or retirement property – preferably both. Lack of assets and cash make their position more difficult. Think broadly – buying property might be obvious solution, but consider buying a plot and building, or approach landlord re surplus estate property?

• Livestock tenants – with herd/flock usually main asset, retirement timing needs to account for market trends to try to get out at the top

• Arable tenants – most of capital is usually in machinery – are depreciating assets a good investment or should farms be using contractors, freeing up capital and investing it off farm?