Getting to grips with the cost of dairy investment

Building a new slurry store or milking parlour can be expensive and fraught with planning and tax hurdles. Suzie Horne gets some advice on likely costs and how best to proceed

An estimated 5000 dairy units need to invest in expanded slurry storage to meet new Nitrate Vulnerable Zone rules by January 2012 or 2013, depending on their area.

While it may seem some way off, farmers need to start planning at least a year in advance of the deadline to ensure they comply in time, warns Richard Davies of DairyCo. “The closer we get to the deadline, the busier contractors will be and you can be sure it will be a bit of a mad rush in those final few months,” he says.

Most dairy units typically have four to eight weeks-worth of storage currently, but this needs to increase to 22 weeks to comply with NVZ requirements, he says.

Often the existing storage will be incorporated into the new design as a reception pit. For a typical 150-cow herd with youngstock and four weeks’ storage that means an extra 2240-2600cu m capacity will have to be built to meet the requirements, costing from £5/cu m to £40/cu m, depending on the type of construction chosen. This represents an investment of between £13,000 and £89,600 before any planning costs.

Where planning permission is problematic, this adds cost and increases the time required to get projects under way.

Mr Davies urges farmers to consider how required storage volumes can legitimately be reduced to bring down the cost of the facility. “At the same time, you need to think about how to future-proof the store. While you may not plan to expand your herd, these requirements will not reduce in future, so consider locating the store so that it could be expanded, and don’t shoehorn it into a space that is only just big enough.”

Example slurry storage costs

Farm details:

150 cows

40 heifers at 12-24 months

40 heifers under 12 months

Current storage 400cu m (four weeks)

Storage requirement calculations take in parlour washings and some yard and roof water

Additional storage requirement is 2240cu m for concrete/steel store or 2600cu m for clay/plastic lined lagoon. Variation is due to the differing regulatory requirement for freeboard (contingency/emergency capacity) once initial storage requirement has been calculated

Freeboard adds another 10% capacity to steel/concrete stores, and another 25% to lagoon type storage because of their greater surface area

For the above example, the cost of storage would be:

Clay lined store: Total construction cost of £13,000 (£5/cu m)

Plastic/HDPE lined lagoon: Total construction cost of £44,200 (£17/cu m)

Concrete/steel store: Total construction cost of £89,600 (£40/cu m)

Planning costs vary widely with the size of store and extent of building work done in the previous two years on the farm

Building project costs often overrun, allow a contingency of 10% in budget, making sure financing arrangements can cope

Building a new parlour

Investing time in the planning process will also pay itself back when building a new milking parlour, says Paul Henman of Promar.

Parlour replacement is all about pounds spent for pounds gained, he says. “You need to decide what your priorities are; one of the main ones will be the rate of cows milked per man hour (or litres per man per hour). You should be aiming for a rate of 75 to 80 cows on that measure.”

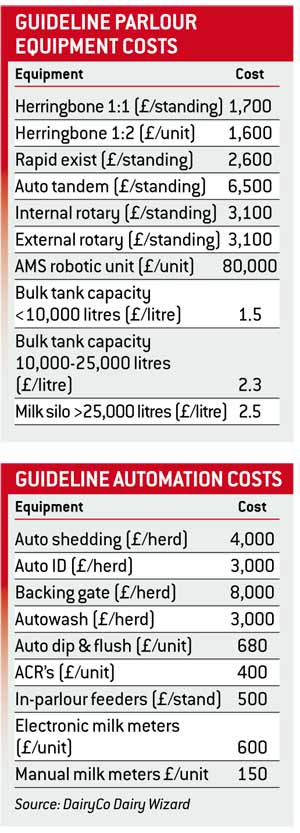

Parlours are one of the items of farm expenditure with the biggest price range for essentially the same job, with herringbone units remaining the most popular choice, he says.

“For our average costed herd size of 189 cows you can get a basic herringbone parlour to achieve 80 cows an hour for as little as £35,000 – this would have no parlour feeding, no Automatic Cluster Removal (ACR), no automation and no milk meters. But you can easily spend £80,000-£100,000 on the same parlour if you are looking at automatic identification, in parlour feeding, ACR, auto-washing and so on.

“I’m not saying you shouldn’t go for extras, but you can spend a lot of money and you might get better records and some efficiency, but it won’t necessarily increase throughput per hour.”

Mr Henman says farmers looking to replace a parlour need to ask some basic questions, such as:

How many people do you want milking?

“A lot of parlours are sold as one-man units but they are simply too big for one man to manage, so don’t be taken in by the sales talk. Go and see one in action – will it really be a one man job in your own situation? With any parlour you need to be clear about the number of people needed in the pit and what is really practical in terms of work routines.

“Do you want a bigger parlour and more people milking at once, or do you want a smaller unit and shift milking? Your parlour routines and yields will also influence your decision.”

Doubled-up or swing-over unit?

“Doubled-up will give you more flexibility with slow milkers, or yield range (ie, if all cows are milked as one group), a swing-over unit will normally cost less but offer less flexibility. Rapid exit-type parlours are worth considering for big herds as the time saved can be worthwhile.”

What level of automation?

“If you’ve always had in-parlour feeders and want them again, is it simply for that reason? Have you really examined what they contribute? Many people now have a feeder wagon so it’s often a bit of a luxury to have in parlour system too. You should put each item of technology through the same scrutiny.

“Rotary parlours are only really suited to very large herds, while robotic units can work very well for smaller herds of 50-60 cows. The problem with robots is that economies of scale are very hard to achieve because they are sold in units costing about £80,000-£100,000 each and when you want to expand or add onto the first unit you can only do it in big ‘lumps’ of expenditure.”

New or second-hand?

“If considering a second-hand parlour, carefully consider labour costs and allow for labour to take a parlour out as well as to put it in. It is unlikely to be covered by any warranty when things don’t work, but it can offer opportunities for the more mechanically-minded farmer.”

In planning a new parlour, think very carefully about cow flow, entry and exit systems and providing an easy way to draft and handle cows, says Mr Henman. The prices are for equipment only, assuming that this is going into an existing building. However, it is rare for parlour equipment to be replaced without additional work being considered, such as backing gates or other alterations to collecting and dispersal areas.

Tax timing is key

The tax treatment of capital investment on farm is complicated and timing is important. Following the phasing out of agricultural buildings allowances – which will completely disappear by 2011 – there is no tax relief on buildings themselves.

However, it is important to distinguish between:

* The building, which attracts no allowance

* Integral features, (eg, electrical or water systems, lifts, conveyors), which attract writing down allowances at 10%

* Plant and machinery within the building, which is eligible for a temporary first year allowance of 40% until 5 April, 2010 (31 March, 2010 for companies) in the year of acquisition with a writing down allowance of 20% in subsequent years

The annual investment allowance of 100% on the first £50,000 of capital expenditure can be applied to the integral features pool or the plant and machinery pool. However, if there are associated businesses or a corporate partner in a farming partnership you may be entitled to only one AIA, or in the case of a mixed partnership, none at all, warns David Missen of Larking Gowen accountants.

“For slurry stores, HMRC has agreed that in many circumstances the entire slurry system will be eligible for capital allowances,” he says. “However one needs to distinguish between a system which is really no more than a hole in the ground, which will not be eligible, compared to a sophisticated system of pumps, filters and lagoons which will normally be treated as plant and machinery, excluding the building or structure.”

On timing of expenditure, the normal rule is that it can be claimed as soon as there is an unconditional obligation to pay. By phasing construction across two tax years it may be possible to maximise the opportunity for relief. However, where the funding is through hire purchase, the asset also needs to be brought into use in the business during the accounting period in which it is claimed.

“If capital expenditure is planned well in the future, consider using a pension scheme to buy or build the asset. This will be more complicated, but in the right circumstances could give 100% relief on substantial sums,” says Mr Missen.