Global competition hotting up in fertiliser markets

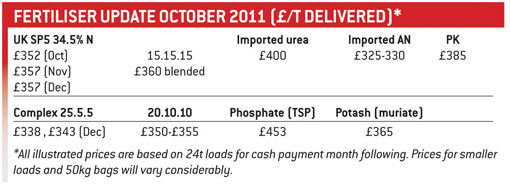

This month has seen little movement of fertiliser and apart from local price fluctuations, little change in pricing. Imported ammonium nitrate remains competitive, however.

It is therefore useful to look at the state of the fertiliser industry before we enter the next tranche of pre-Christmas activity.

Some farmers recall the days when three manufacturers, UKF, ICI and Fisons slugged it out to provide UK-produced nitrogen. The perception was this provided competition and fair prices. The reality was that because of high UK energy costs, nitrogen pricing here was higher than many other parts of the world. Ironically the introduction of cheaper imported urea was the catalyst for the rapid contraction of the UK manufacturing base, and the western European fertiliser industry.

The UK was left with left just one nitrogen producer, GrowHow, a 50:50 joint venture between CF Industries Holdings and Yara International ASA. Its two British ammonia plants produce ammonium nitrate and granular compound fertilisers, supplying 40% of Britain’s nitrogen needs, with a significant proportion sold to other UK fertiliser suppliers. It can also import and export ammonia or finished products.

Co-owner, Yara, has a substantial wholesale business in the UK, also selling ammonium nitrate and compounds imported from Europe.

The remaining nitrogen comes from around the world, as ammonia, urea or ammonium nitrate, usually from locations where energy prices are significantly cheaper. Quality, once the bugbear of these imports, is increasing all the time and two recent developments are set to increase competition within European markets.

The first of these was the announcement that OCI (Orascom Construction Industries), one of Egypt’s largest corporations, has purchased the fertiliser interests of Dutch Giant, DSM.

Nassef Sawiris, chief executive of OCI, said the acquisition would allow OCI to expand its customer base in key European markets, with a range of products including urea, ammonia, calcium ammonium nitrate, urea ammonium nitrate, and ammonium sulphate.

Secondly, in a €700m deal announced last month, BASF agreed to sell its Antwerp fertiliser interests to EuroChem of Russia.

EuroChem chief executive Dmitry Strezhnev said the deal would provide it with “significantly improve its proximity to European customers”.

Add to that the growth aspirations of Uralchem, already trading in the UK, and we have three giants on our doorstep with access to lower priced energy. This puts the global market shares of GrowHow (around 0.5%) and Yara (7-8%) into perspective. Indeed the UK demand for nitrogen is less than 1% of the total world market.

In fact, 60% of our nitrogen, all our phosphate, 30% of potash and almost 90% of sulphur is imported.

The blending industry in Britain is well established and supplies not only NPK and S fertilisers but also straight N, P and K, usually on a regional basis. Many of these companies are long established and have local knowledge and the ability to supply custom mixes for special crops. “Delivered and spread” is a popular service.

Blenders include; Law’s, East Anglia; PB Kent, Immingham; McCreath, Simpson and Prentice, Berwick; J & H Bunn, Norfolk; Carrs Fertiliser, Carlisle and Scotland; CFS, Goole; Soil Fertility Dunns, Ayr; Mole Valley Farmers, Devon and Wynstay Farmers, Powys.

This summer Carrs Fertilisers was acquired by Origin Enterprises, making the company part of a much larger group with leading market positions in the supply of agronomy, crop nutrition and feed ingredients. PB Kent and Gouldings is also part of the group.

Earlier this year Kansas-based Koch Fertiliser acquired J & H Bunn. Koch and its subsidiaries have the capacity to manufacture, market and distribute 10m tonnes of fertiliser per annum, making them one of the world’s largest suppliers.

There is no phosphate industry as such in the UK. The two markets we have, straights for the farmer and intermediates for the manufacturer, rely on successfully trading imports of superphosphates from Bulgaria, Morocco, Tunisia, Poland and Finland. Mon- and Di-ammonium phosphates come from Russia.

ICL of Tel Aviv is typical of the kind of multi-billion corporation involved in the mining and marketing of P and K. Cost of phosphates is largely determined by supply and demand and small companies in Britain have little bargaining power.

ICL also owns our own UK potash mine, Cleveland Potash, which produces over 1m tonnes per annum. Europe’s largest producer is probably K&S of Germany with other supplies from Russia.

Competition may be increased if developments of the Boulby mine in Yorkshire go ahead, an enterprise recently acquired by Sirius Minerals, with interests in Australia and North America.

Another sector of our UK fertiliser marketplace which is slowly expanding and possibly now accounts for as much as 25% of our nitrogen usage is that of liquid fertilisers. The two major players are Chafer, the brand name of Yara’s liquid fertiliser range, and Omex. Both largely rely on imported intermediates to produce their products.