Wheat prices have a direct link to farm values

As we head into autumn, the UK farming industry is holding its breath. It looks as though we are facing imminent recession on a global scale and the wettest August on record has meant that those farmers who managed to get harvest in and incurred the additional costs of drying grain were the lucky ones – those that didn’t stand to lose their crops entirely.

Private investment in the agricultural industry through international soft commodity markets has increased from £10bn in 2003 to £150bn in 2008. Aggressive investment into this sector has magnified the volatility in the markets, caused by a number of factors such, as grain stocks being at their lowest for 20 years.

But while high UK yields have been predicted, harvest has been exceptionally difficult and the quality poor. This may drive down prices, but could also increase the differential between feed wheat and milling wheat.

This is relevant to the land market, thanks to the increased number of investors buying land (27% of farms sold to the end of August compared with 16% for the whole of 2007), resulting in the price of land now more closely linked to wheat values than to house prices.

This is relevant to the land market, thanks to the increased number of investors buying land (27% of farms sold to the end of August compared with 16% for the whole of 2007), resulting in the price of land now more closely linked to wheat values than to house prices.

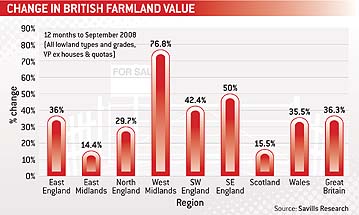

UK farmland rose in value by 30% last year alone and so far this year we have seen a 29.6% increase in values up until the end of July. This has been linked to tight supply, but it looks likely that there will be a large amount of land coming to the market this autumn.

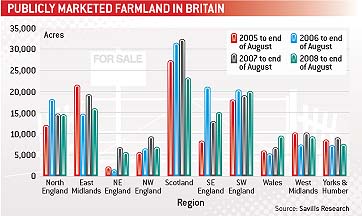

As at the third week of September we have 40,700 acres either available or in the pipeline for autumn, of this approximately 50% is being offered privately. This private market, which historically accounts for about 10% of the farmland market, has grown as purchasers are looking to take advantage of increased values and the presence of a few large, acquisitive parties known to be active in the market.

With this anticipated increase in supply, we are already seeing that growth is slowing and values have levelled out while the “froth” in the market is receding leading to values at more sustainable levels of about £6000/acre.

The best farmland is still commanding the highest prices and we are seeing a two-tiered market developing, with high quality, productive land (with little or no residential property) achieving premium prices while poorer quality units remain static.

Central England

After sharp increases in farmland values over recent years it appears that farm and land values in the central region, like elsewhere, have plateaued. However, a continued lack of supply and a flight to quality property by purchasers has enabled us to conclude a number of very successful sales at values well over £6000/acre for blocks of commercial land.

Residential and sporting farms continue to sell well but there has been a definite refocus of our applicant base towards commercial land and farms. The recent sales of Elm Bank Farm near Stow-on-the-Wold, Gloucestershire and Astwood Grange Farm, Buckinghamshire, have shown that there is still a broad range of active purchasers looking to buy, from City-based residential buyers and investors to local expanding farmers and farmers relocating from elsewhere.

We are expecting more farmland to come to the market this autumn and, despite a very difficult harvest, we see no reason for the demand for quality farms and land to wane.

Southern England

The farmland market in the south is different to this time last year. With such a wet harvest, continual poor economic forecasts and a meltdown in the housing market it is unsurprising that last year’s values of between £6000 and £7000/acre have eased. While we are not seeing a decline there is more reluctance to commit to these levels by purchasers.

There is still a demand, however, for quality commercial farms, although a more muted appetite for the large house. Deals are taking longer to achieve and exchange. Good farms will always sell but sellers have to be realistic.

There is still a demand, however, for quality commercial farms, although a more muted appetite for the large house. Deals are taking longer to achieve and exchange. Good farms will always sell but sellers have to be realistic.

With two medium-sized commercial farms, one a 600-acre dairy in Somerset and the other a 500-acre arable farm in Hampshire, due to be launched this month, I am confident we shall see good interest, but not quite at 2007 levels.

Yorkshire and the north east

The market in Yorkshire continues to be dominated by lack of supply and there are few signs of this changing this autumn.

There have only been two commercial farms in excess of 300 acres marketed all year in the county, which is really frustrating for purchasers. Further north and west there has been more activity, particularly in Northumberland where there will be almost 10,000 acres available by the end of this month although dominated by two large sales.

Values rose strongly in the first quarter to about £7000/acre for the best land with many transactions between £5000 and £6000/acre. I generally believe that the market has peaked as a result of falling wheat prices and rising input costs.

The extreme harvest conditions have affected optimism and profitability, but there is no evidence yet that values have been affected in Yorkshire. There will continue to be good demand for well-equipped commercial farms in areas where volume remains restricted.

Scotland

Since the move to the single farm payment system in January 2005, land prices in Scotland have risen by 78% across all land types. This figure includes a near 100% rise in the value of prime arable land.

Since the move to the single farm payment system in January 2005, land prices in Scotland have risen by 78% across all land types. This figure includes a near 100% rise in the value of prime arable land.

The main drivers behind this increase have been a shortage of acres for sale, an expectation of rising global product prices in the world market and non-farming money looking for a safe haven.

This autumn, with these three “drivers” beginning to flag, (bar the beef price which is now approaching 300p/kg) a pragmatic buyer might consider that values should plateau until a new source of momentum comes forward – another grain shortage, interest rates lowered, inflation up, world unrest? Either way, in a market which is unsure of its direction, the flight is always towards quality.

We expect prime arable acres in Scotland to trade at more than £6000/acre, while a wider gap opens up between this top quality land and the rest. Also, with the euphoria over biofuels calming down and the grain speculators moving on to other commodities again, it is easier to see why more land might come to the market this autumn or next spring.

Buyers who were considering selling in 2005 and 2006 who held off to gain from the promise of increasing profits and higher land prices may, following one of the wettest Augusts in memory, decide that they should proceed with their earlier plans. Either way, I am confident that Scotland’s land market will remain robust through to 2009.

East Anglia

Land prices in East Anglia are holding on to the gains over the year to date, though in some places there is beginning to be evidence of more caution.

Overall demand is still strong from farmers and investors for good land, with values currently ranging between £5500 and £6250/acre for reasonable quality cereal land, and up to £6500/acre for irrigated sand land suitable for vegetable production.

Overall demand is still strong from farmers and investors for good land, with values currently ranging between £5500 and £6250/acre for reasonable quality cereal land, and up to £6500/acre for irrigated sand land suitable for vegetable production.

Farms with residential elements are now more patchy with quality selling well. Long-term, the outlook looks positive but there may be a slight short-term cooling, as the market draws breath.

There has been a surge in supply in the east this autumn and judging by the response, plenty of demand. They include two estates in Norfolk, the largest of which we are selling privately. It’s rare to get the opportunity to buy an estate so premiums are paid by the seriously rich. Shortly to launch are a clutch of commercial farms, including a grade 2 top-quality 1400-acre unit in Hertfordshire and 600 acres of irrigated vegetable land in west Norfolk, both of which Savills have had buyers competing to try and buy before they are marketed.

Return to Property special homepage