Machinery investment dilemma – should you buy or use a contractor?

It’s a familiar dilemma for many farmers – carry on using a contractor or buy your own machine. Suzie Horne asked the experts to suggest the best way forward

Andrew Porteous farms in partnership with father Ian at Lea Fields Farm, Shutt Green near Brewood, Staffordshire. They milk 110 cows and keep a further 110 youngstock, producing their own replacements and taking bull calves to 7-8 months old.

For many years Mr Porteous has used contractors to bale his hay and the straw on a nearby farm, in exchange for muck. However, after a bad experience last year left him with poor-quality bales, he has been considering buying a secondhand baler but is not sure he can justify it for 700 round bales a year.

FW asked The Dairy Group‘s Ian Powell to assess the proposition.

“The best way to approach a decision such as this, where you are considering investing in an extra machine rather than a straight replacement such as a tractor, is to do a partial budget,” says Mr Powell.

A partial budget compares the extra costs a business will incur if it makes a change against the costs saved by the move. It must include all relevant costs at realistic rates.

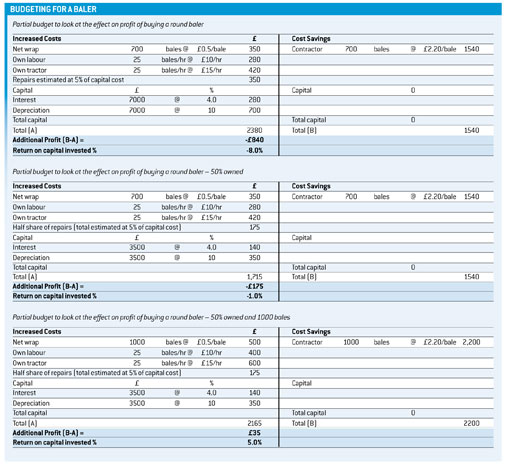

In this case, spending £7000 on a secondhand baler to make 700 bales a year compared with paying a contractor £2.20 a bale to do the job would leave Mr Porteous £840 worse off, showing a -8% return on the capital invested (see table 1). This assumes service, repair and insurance costs at £350 a year.

Putting the correct values on your own or employed labour, tractor charges and work rates is crucial. Here the rate used is 25 bales an hour with labour at £10/hr and tractor costs at £15/hr.

Many might think that they can offer a tractor and driver for less than £25/hr, but they should look again at their true operating costs, says Mr Powell.

“It is also important to remember depreciation. The rate used in the partial budget is relatively low at 10% – a safer assumption might be 15%,” he suggests.

In some cases the cost of the investment can be reduced by sharing ownership or costs with a neighbour. Owning a half share for making 700 bales brings the loss down to £175 with a return of -1% on the capital invested (see table 2).

While acknowledging that there can be strong practical reasons for owning kit rather than using contractors, Mr Powell reckons that 1000 bales would be the minimum volume to make this investment worthwhile. Even on a shared machine, this would give just a £35 benefit in additional profit and a 5% return on capital (table 3).

For the time being, putting in cubicle mats at Lea Fields Farm is the priority for the capital expenditure budget but, having gone through the partial budget exercise, Mr Porteous is considering buying a secondhand baler next year to gain timeliness and control. He has a nearby farm in mind which may share the purchase and running costs or give him contracting work.

“The partial budget is a very good way to test the effect of a decision on the business – I probably wouldn’t have approached it that way but will use it again in the future. There’s not much in it financially but there is a lot to be said for having your own machine,” said Mr Porteous.

“We have an excellent self-employed fitter, Peter Darlington, for any repairs. We rarely buy new machinery but are very careful what we buy, which is good secondhand kit with names that hold their value well. We look after the machinery well so this baler should still be worth a fair bit in five years’ time.”

Weighing up machinery investment

“With any purchase or change, you have to ask yourself: What is driving the decision? Why are you changing and what will you gain? On most farms it is not particularly well planned,” says Mr Powell.

“When you are replacing a front-line tractor, for example, it’s a fairly straightforward case – you need reliability and so you should probably be thinking of replacement once a key tractor gets to 5000-6000hr.

“Where you are considering an additional machine rather than a replacement, then use a partial budget to calculate the effect on profit to help you make the right decision.

“You also need to consider the impact on workloads, cash-flow, borrowing requirements and the timing of any investment as this is likely to have a tax impact.

“But beware of using the argument that you will pay more tax if you don’t invest. In many cases it is better to have the money in the bank and pay the tax.”

Be careful also about justifying the decision on the basis that you might get contracting work. If this is part of the equation, you need to be sure of the work, rather than trying to find it once you have bought machine, says Mr Powell.

The finance options will usually be overdraft, loan or hire purchase.

“With base rates so low, overdraft borrowing would be the obvious choice, with most farmers paying a margin of 1.5-2.5 points over base rate and arrangement fees of 0.5-1% giving an actual annual rate of 2.5-4%.

“A loan (fixed or variable) might be used for larger machinery items repaid over 3-5 years.

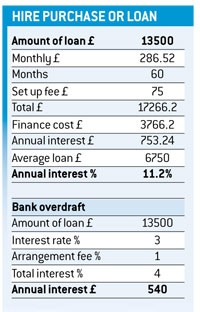

“HP is the third option but beware – it tends to be far more expensive than overdraft. In a case I came across recently, the HP cost of a facility of £13,500 worked out at 11% interest compared with the bank overdraft which was 4%. This gives a difference of £1065 in interest costs over the five years of the loan.

“You also need to know the basis of any offer. Lenders should tell you what the APR is and you must also be clear about any set up or arrangement fees.

“You can work out the approximate annual rate of interest by calculating the average size of the loan. In the example this is £6750, which is the original loan of £13,500 divided by two because you will have paid half the loan off by the halfway point of the term.”

The next step is to divide the annual interest cost (£753) by the average loan (£6750), which gives you an annual interest charge of 11.2%. Having this figure allows you to compare the cost of finance sources.

Do you have a machinery investment dilemma you’d like us to call in the experts for? Email a brief summary to david.cousins@rbi.co.uk