Eggs and poultrymeat head in opposite directions

Since the start of 2010, both the egg and poultrymeat sectors of the UK industry have been expanding strongly, and both have had to contend with extreme rises in the cost of rations.

However, their fortunes have gone in opposite directions.

The egg sector has experienced a severe bout of overproduction, combined with a large structural imbalance in terms of the kinds of eggs being produced.

For the poultrymeat sector, there has been steady expansion guided by the integrators to meet growing demand. Prices have remained favourable and some much-needed reinvestment has been taking place.

Even the declining turkey industry appeared to turn a corner in 2010.

Over the following pages our annual Facts and Forecasts feature takes a detailed look at trends in all sectors of the industry over the past 18 months, and anticipates where things might be heading at the end of 2011.

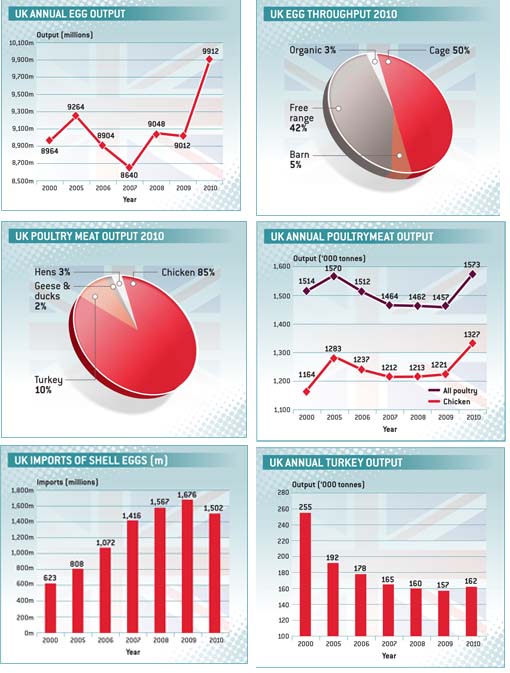

EGGS

Free-range egg producers have endured one of the toughest 18 months since the start of the modern industry, and ironically it is next month’s ban on conventional cage production that is the underlying cause.

Brussels’ move to end this type of production feels like it has been a long time coming, yet despite all the warnings for the industry to prepare, managing the transition to the new regime has turned into a messy affair.

Two tricky fundamentals have had to be resolved at the same time: what balance to aim for between enriched cages and free range once 2012 arrives; and how to phase in the replacement production units – whether free range or enriched – without disrupting the market. Arguably the industry got it wrong on both counts.

The latest figures in this feature relate principally to 2010, the last full year for which any of the data are available. And these figures show that the troubles in the market started in 2010. It takes a long time to bring in new capacity, especially for free range, given the complexities of finding suitable new producers, gaining planning permission, securing finance and then bringing the new unit to completion.

Hence it was unsurprising that the new capacity started to come on stream in good time, during 2010, and this occurred long before any corresponding downturn in cage production. As a result, the overall growth in output that followed was probably unprecedented in the history of the egg industry.

As the first line of Table 1 shows, total output for human consumption rose by 900m eggs from 2009 to 2010 as a whole, a rise of 10%. Cage production remained unchanged, so all of this increase was accounted for by alternative systems: around 100m for barn, and 800m for free-range production.

Taken over three years, from 2007 to 2010, free-range production rose by a massive 70% or 1.6bn eggs a year.

There was virtually no change in uptake by the egg processing sector in 2010, so all of the additional eggs went forward as shell eggs. There was a 10% rise in exports of eggs and egg products, but quantities in this sector are so small that only 24m extra eggs were shipped off the beleaguered UK market.

A significant volume of imports of eggs and products was choked off, dropping by around 250m eggs, but the net result was still a rise in the number of eggs reaching the market of 625m, an increase of over 5% compared with 2009.

A surge in supplies of this order would always be more than the market could stand, and the inevitable result was a price slump that has persisted right through 2011.

During 2010 the average free-range producer price was down 6p to 84.4p/doz, compared with 90.2p in 2009. Cage prices were less affected, and fell by around 2p to 53.6p/doz.

However, the figures in the table reflect average prices over the year, and in fact producer prices did not reach their peak until the first quarter of 2010 at 91.3p/doz (57.5p for cage). At the other extreme, by the end of 2010, the price during the last quarter was down to 83.8p/doz for free range (52.8p for cage).

Prices went on falling, and finally bottomed out in the second quarter of this year, at 82.2p/doz for free range and 52.2p for cage. Although the cage market was never in surplus, the whole industry has had to bear the cost of “cascading” eggs down from the free-range sector into cage simply to find buyers.

All this took place against a background of rocketing feed costs. There are no feed prices in the accompanying tables, but the chart of Poultry World‘s basic layers ration on p20 tells the story: feed costs peaked in February this year, just before producer prices reached their lowest point. Between June 2010 and February 2011, the cost of a basic ration rose by nearly £100 from £182/t to £274/t.

With feed costs rising and egg prices falling on this scale, producers have struggled to stay afloat and there were fears that the recent new entrants would be unable to survive even until the cage ban came into effect.

However, the pressure has eased considerably since the early part of this year, particularly on feed costs which have dropped back to around £210/t this autumn. Producer prices have also started to inch upwards, although by the third quarter they had only gained about 0.5p/doz on free range compared with the previous quarter.

With just a month to go before the cage ban comes into force, very few conventional cage units are still in production in the UK, and the market is back into reasonable balance overall. Supplies have begun easing back and in the third quarter this year, packing station output fell below the level of a year ago for the first time in two years.

What is still unclear is whether the current balance between enriched cage, barn and free range is a true reflection of what the marketplace requires. If it isn’t, it will be hard to raise producer prices in the free range sector by much in the near future.

All eyes will be turned across the Channel as 2012 gets under way and the cage ban begins. It is widely accepted that many member states are unready for the ban, and industry leaders will be attempting to monitor the movements of any traditional cage eggs that continue to be produced across the EU.

However, it is unlikely that there is an overall surplus of free range or enriched cage eggs in the EU for export to the UK, and if conventional cage eggs can be confined to their country of origin, or at least successfully kept out of the UK, there should be an opportunity for some producer price increases in 2012.

POULTRYMEAT

Higher feed costs have not deterred the continued expansion of the poultrymeat sector in the UK over the past 21 months.

Total output was up by 8% in 2010, according to the latest full-year figures from DEFRA. This added 116,000t to the annual production figure, taking it past the 1.5m tonnes mark and back to the level of five years ago.

Imports have been rising as well, surging ahead by more than 50,000t in 2010. With exports little changed, overall UK consumption rose by 160,000t last year, and per capita consumption was up by 2.5kg.

The broiler industry has spent the last couple of years recovering from a downturn caused by poor returns and ageing housing stock, with many producers leaving the sector. Producers are now returning to the industry, or entering for the first time, and total production of broiler meat broke a new record in 2010, to pass 1.3m tonnes for the first time. Similarly, day-old chick placings passed 900m for the first time in 2010, after showing an annual increase of 60m, or 7%. Slaughterings rose by a corresponding amount.

The turkey sector has followed a different pattern, having contracted throughout the decade, but finally reaching a low point in 2009 before showing a rise in output of 3% last year.

Over a five-year period, broilers were up 40,000t, turkeys down 30,000t, and ducks and geese also down by 10,000t, putting total production in 2010 on a par with 2005.

In more recent months the rate of growth for broilers has steadily slowed, but this could be as much to do with the difficulties of quickly establishing new capacity, as any increased pressure on profitability from higher feed costs.

During 2011, monthly broiler chick placings have shown a year-on-year rise of 1%-3%, while the rolling 12-month total up to September was 4% higher than in the previous period.

In the turkey sector the recovery trend has been accelerating, with double digit growth in day-old poult placings in every month of this year. March and May saw year-on-year rises in poult numbers of 23%.

Accordingly, the rolling 12-month placings total has shown a rising trend and stood at 13% in September, making it the most bullish year for turkey numbers for more than a decade.

As a result, production of all poultrymeat has been increasing during 2011, and by September the moving 12-month total stood at 1.58m tonnes. This represents a rise of 60,000t on the year to September 2009, so that poultry output is on course for a total increase of around 4% this year.